Artificial intelligence, once a gentle tailwind for U.S. economic growth, has transformed into a powerful, hurricane-strength force reshaping the entire economy. Its pervasive influence is now distorting the stock market, corporate profits, the pace and nature of economic expansion, international trade, and even public sentiment, particularly concerning the job market.

Artificial intelligence, once a gentle tailwind for U.S. economic growth, has transformed into a powerful, hurricane-strength force reshaping the entire economy. Its pervasive influence is now distorting the stock market, corporate profits, the pace and nature of economic expansion, international trade, and even public sentiment, particularly concerning the job market.

The sheer omnipresence of AI makes it increasingly challenging to accurately assess the current economic landscape. It is overshadowing the impact of other significant events, such as trade tariffs and geopolitical conflicts, which would ordinarily be considered major economic disruptors in their own right.

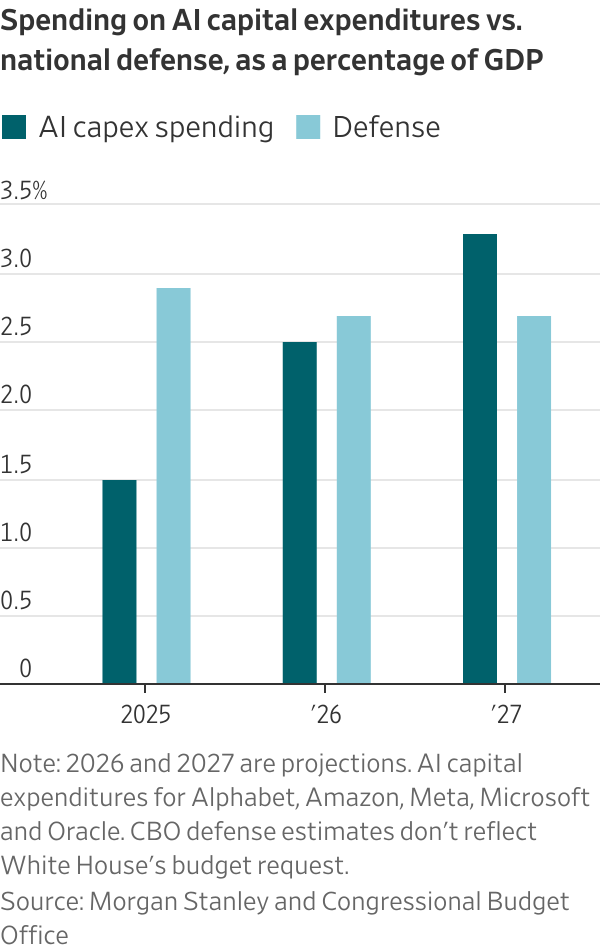

The current economic boom driven by AI is venturing into uncharted territory. Projections indicate that capital expenditures by the five largest AI "hyperscalers" are expected to exceed $800 billion this year and are forecast to reach a staggering $1.1 trillion next year. This figure, representing 3.3% of the gross domestic product, would surpass projected national defense spending.

This unprecedented surge prompts a critical question: What if the AI boom, specifically the accompanying frenzied investment and spending, were to subside? While the underlying AI technology is undeniably here to stay, the current speculative fervor might not be.

This unprecedented surge prompts a critical question: What if the AI boom, specifically the accompanying frenzied investment and spending, were to subside? While the underlying AI technology is undeniably here to stay, the current speculative fervor might not be.

The conventional wisdom suggests that an AI bust would precipitate an economic collapse. However, upon closer examination of the distortions AI is currently creating, this outcome is not as certain as it might appear.

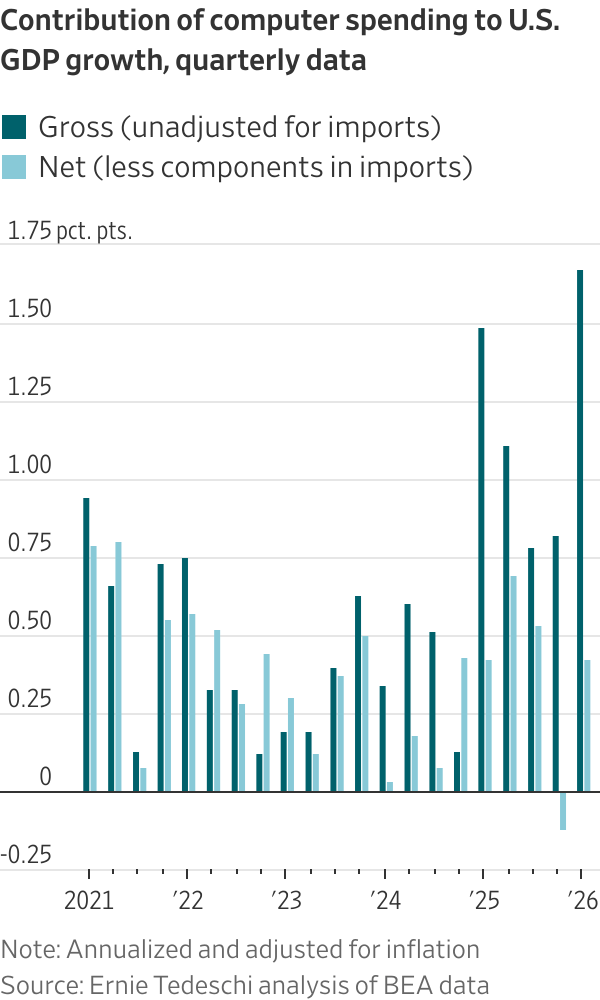

To begin with, let's consider the broadest measure of economic growth: inflation-adjusted GDP. In the first quarter, it registered a respectable 2% annualized growth. Yet, beneath this aggregate figure, two distinct economies are at play: the AI-driven sector and the rest of the economy.

Personal consumption, the largest component of GDP, exhibited more moderate growth at 1.6%. Investment in areas such as housing, business structures like office buildings and factories, and transportation equipment including trucks and aircraft, experienced declines. Conversely, investment in tech equipment surged by 43%, software by 23%, and data center construction by 22%.

A back-of-the-envelope calculation suggests that the AI economy grew by an impressive 31%, while the non-AI economy expanded by a mere 0.1%. David Sacks, who served as President Trump's AI czar, has predicted that AI will contribute an additional 2 percentage points to economic growth this year.

However, it's crucial to acknowledge that while AI is influencing economic growth, its own contribution is subject to distortions. A significant portion of AI-related spending is directed towards imported equipment, such as advanced semiconductors, rather than domestic production. Ernie Tedeschi, chief economist at Stripe, employing a more sophisticated analytical approach, calculated that gross computer spending accounted for 1.7 percentage points of the first quarter's 2% GDP growth. When the impact of imports is netted out, this contribution diminishes to just 0.4 percentage points.

This observation highlights another area that AI is significantly distorting: international trade. This is a primary reason for the substantial increase in U.S. imports during the first quarter, which in turn widened the trade deficit. It also explains Taiwan's trade surplus, which has reached an almost unimaginable 24% of its GDP. The Kospi, South Korea's stock index, home to semiconductor giants like Samsung Electronics and SK Hynix, has seen a remarkable 78% increase this year. Therefore, while former President Trump aimed to reduce the U.S. trade deficit and other countries' surpluses through tariffs, the opposite is occurring due to the AI phenomenon. Without the influence of AI, his tariff policies might have yielded different results.

This observation highlights another area that AI is significantly distorting: international trade. This is a primary reason for the substantial increase in U.S. imports during the first quarter, which in turn widened the trade deficit. It also explains Taiwan's trade surplus, which has reached an almost unimaginable 24% of its GDP. The Kospi, South Korea's stock index, home to semiconductor giants like Samsung Electronics and SK Hynix, has seen a remarkable 78% increase this year. Therefore, while former President Trump aimed to reduce the U.S. trade deficit and other countries' surpluses through tariffs, the opposite is occurring due to the AI phenomenon. Without the influence of AI, his tariff policies might have yielded different results.

Impact on Stocks and Profits

One of the key reasons why rising energy prices have not derailed the S&P 500 from reaching new highs is the resurgence of the "Magnificent Seven," a group of technology companies that collectively represent over a third of the index's market capitalization. This sector has experienced a significant rebound, with the index up 7% since the commencement of the conflict in Iran. If all 500 companies in the index were weighted equally, the index would have actually experienced a slight decline.

The "AI reality distortion field" extends beyond the Magnificent Seven. Intel's stock price recently surpassed its all-time high, which was set during the dot-com bubble in 2000. This surge is not indicative of the company overcoming its strategic challenges; rather, it is struggling against Nvidia in the crucial area of graphical processing units (GPUs), which are essential for AI, and against Taiwan Semiconductor Manufacturing Co. in chip manufacturing for external clients. Instead, the demand for central processing units (CPUs), Intel's area of specialization, from data centers has been exceptionally strong. A similar positive effect has benefited the entire semiconductor sector, including companies like Advanced Micro Devices, Micron Technology, and Sandisk.

The distortions caused by AI are not limited to stock valuations but also significantly impact corporate profits. FactSet estimates that total S&P 500 earnings are on track to increase by a substantial 27% in the first quarter. However, the profits for the Magnificent Seven alone are projected to rise by 61%, while the remaining 493 companies in the index are expected to see a more modest 16% increase, a figure that is itself boosted by semiconductor companies like Micron.

Widening Gap Between Capital and Labor

This trend is skewing the distribution of economic gains between capital and labor. As corporate profits surge, labor compensation, which includes wages and benefits, grew at a slower pace of 3.1% annualized in the first quarter. The Labor Department reported that after accounting for inflation, labor compensation actually shrank by 0.5%. Consequently, labor's share of total business-sector output has fallen to 54.1%, marking the lowest point since records began in 1947.

AI, therefore, contributes to the disconnect between what economic data suggests and how individuals perceive their financial well-being. It boosts the optimism of businesses and investors while having the opposite effect on ordinary workers.

Scientists and corporations continue to highlight the tasks that AI can perform more efficiently than humans. Simultaneously, companies announcing layoffs, such as Coinbase and Snap, frequently cite the increased efficiencies gained through AI adoption. According to Gallup, 23% of employees at companies implementing AI anticipate their jobs being eliminated within five years. This pervasive concern about job displacement might be a contributing factor to subdued wage growth, as employees may be less inclined to demand raises if they fear being replaced by automation.

However, this widespread sense of gloom might itself be another form of distortion. While some studies predict job losses due to AI, concrete evidence remains scarce, even in sectors considered vulnerable, such as software development. In reality, private-sector layoff announcements are currently running below the levels observed a year ago. Furthermore, companies attributing job cuts to AI might find it a more palatable explanation than admitting to internal management failures.

The Potential Impact of a Cooling AI Market

Imagine a scenario where the global appetite for AI spending abruptly diminishes, leading to the dissipation of the current boom. In such a situation, we would likely witness an economy free from the distortions currently imposed by AI, but not free from the technology itself.

Overall U.S. economic growth would undoubtedly slow, but perhaps not as dramatically as one might expect. Given that a significant majority of data centers are concentrated in just 33 counties, a substantial reduction in data center construction would not have a widespread ripple effect across the nation.

Stock markets and corporate profits would likely decline. However, the average worker, whose financial well-being is more closely tied to wages than to investments, would experience minimal direct impact. Moreover, public sentiment might improve if business leaders were to reduce their emphasis on AI-driven automation.

No comments:

Post a Comment