Apple has made significant strides in the AI space with its latest announcement at the Worldwide Developers Conference (WWDC). The company unveiled the next iteration of Apple Intelligence, which includes a more advanced version of Siri powered by next-generation Apple Foundation Models. These models are developed in collaboration with Alphabet's Google Gemini, highlighting Apple's commitment to integrating cutting-edge AI into its ecosystem.

Despite these advancements, the market's reaction was relatively muted, with Apple's stock trading in the red on June 9. This suggests that investors are cautious about how quickly Apple can convert its AI innovations into tangible revenue growth. While the company has shown ambition, the financial impact of these developments remains uncertain in the short term.

One of the most promising monetization strategies for Apple lies in its subscription model. The company revealed that certain features of Apple Intelligence, such as AI-powered image generation, will have daily usage limits due to their reliance on resource-intensive cloud-based models. Users who wish to access more extensive capabilities can do so through eligible iCloud+ subscription plans. This approach not only encourages users to upgrade their subscriptions but also creates an additional revenue stream for Apple.

Another potential revenue driver is the iPhone upgrade cycle. The new Apple Intelligence features and enhanced Siri AI experience will be available exclusively on the iPhone 16 models and newer, as well as the iPhone 15 Pro and iPhone 15 Pro Max. This means that millions of existing iPhone users will need to upgrade their devices to access the full range of AI capabilities. As a result, Apple could see a boost in hardware sales, especially among customers looking to stay up-to-date with the latest technology.

These developments present two key opportunities for Apple: increased subscription revenue and accelerated hardware sales. However, the market's cautious response indicates that investors remain skeptical about the near-term financial impact of these initiatives. While the long-term potential of AI is significant, monetizing it at scale will likely take time and continued investment.

When evaluating whether Apple stock is a buy, hold, or sell, it's important to consider the company's strong fundamentals. Despite the market's cautious reaction to the latest Siri AI announcements, Apple's investment case is supported by resilient iPhone demand and the continued expansion of its highly profitable Services business.

Apple delivered an impressive first half of 2026, with double-digit revenue growth. This growth was achieved despite higher memory costs, showcasing the company's ability to manage expenses while maintaining pricing power. In the second quarter of 2026, revenue reached $111.2 billion, a 17% increase year-over-year (YOY). The iPhone remained the primary driver of this growth, generating $57 billion in revenue, a 22% YOY increase despite ongoing supply constraints.

Demand for the iPhone 17 lineup remained robust across major markets, including the U.S. and Greater China. Apple also reported record levels of active iPhone users and a new March-quarter record for device upgrades. These metrics indicate that Apple's hardware business continues to benefit from a loyal customer base and a strong replacement cycle.

While iPhone sales continue to drive revenue growth, Apple's Services segment is increasingly contributing to profitability. The company now has over 2.5 billion active devices worldwide, providing a solid foundation for recurring revenue through subscriptions, payments, cloud services, and digital content. During Q2, Services revenue grew 16% YOY to $31 billion, with double-digit growth across most geographic regions and business categories.

More importantly, the Services segment is enhancing Apple's margin profile. Overall gross margin improved to 49.3%, while Services gross margin expanded to an impressive 76.7%. In contrast, product gross margin declined to 38.7%, underscoring the growing importance of Services as a profit engine. As Services becomes a larger portion of total revenue, Apple should benefit from stronger earnings growth and greater resilience during hardware cycles.

Key Risks Investors Should Watch For

While AI-driven revenue opportunities may take time to materialize, Apple's strong iPhone demand, ecosystem strength, customer loyalty, installed base growth, and expanding Services business remain the primary drivers of shareholder value.

That said, investors should remain aware of two key risks. Rising component costs could pressure hardware margins. Additionally, the current valuation already reflects significant optimism about Apple's future performance.

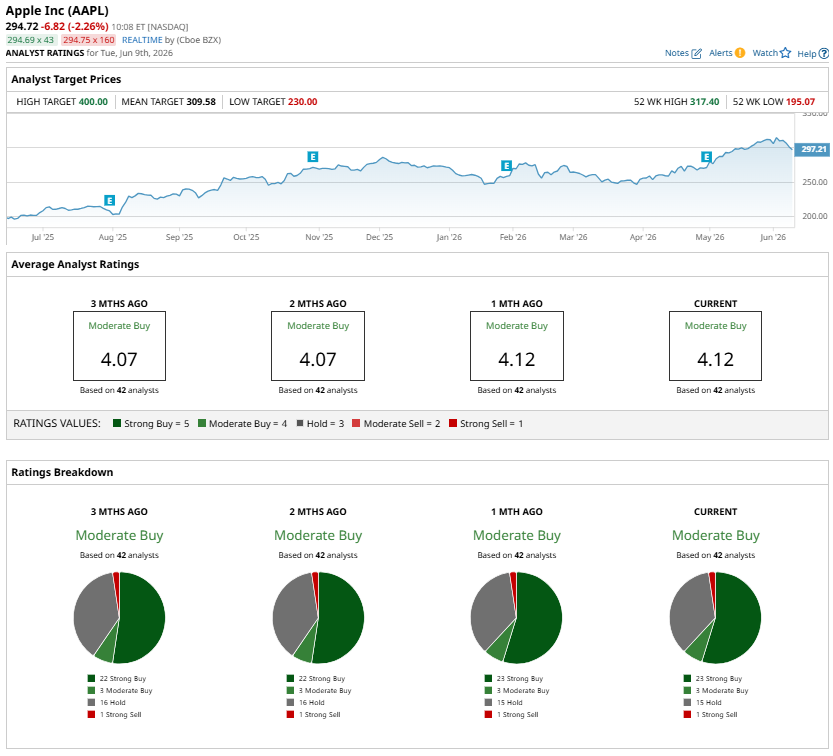

For existing shareholders, Apple remains a compelling long-term hold. However, the valuation suggests that positive outcomes are already priced in, and new investors may want to wait for a better entry point. Analysts currently rate AAPL stock as a consensus "Moderate Buy."

On the date of publication, Amit Singhdid not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Disclosure Policy here.

More news from ・Quantum Computing Looks Like Nvidia in 2019. This Could Be the Generational Buy of the Decade. ・A Short Squeeze Is Underway in Cracker Barrel Stock. What to Know. ・Dear Flex Stock Fans, Mark Your Calendars for June 22 ・The $7 Billion Reason Super Micro Computer Stock Is Down Today Get exclusive insights with the FREE Brief newsletter. Sign up for a midday guide to what's moving stocks, sectors, and investor sentiment. Subscribe today!

No comments:

Post a Comment